Hot Inflation Data Jolts Investors

For nearly a year, investors have had the late spring/early summer months circled on their calendars for a potential jump in inflation. Base effects from rolling off weak data a year ago held the promise of eye-popping year-over-year numbers, and an economy that would be increasingly reopening meant inflation could start to run hotter month over month. Still, today’s inflation numbers came with some serious sticker shock.

The U.S. Bureau of Labor Statistics released its monthly report on inflation this morning, May 12, revealing that the headline Consumer Price Index (CPI) rose 0.8% month over month and 4.2% year over year. The core CPI, which strips out food and energy, rose 0.9% month over month, its highest reading since the early 1980s, and 3.0% year over year.

Given the base effects from a year ago, we view the month-over-month changes as much more informative for the inflation outlook. Used car and truck prices surged 10% in April, their largest gain ever and representing the largest contributor to the overall rise, while other components seeing large jumps month over month included lodging away from home and airfare. Major CPI components, though, such as rents (0.2%), showed much more moderate rises.

“Today’s data release is only going to escalate the market’s focus on inflation,” explained LPL Financial Chief Market Strategist Ryan Detrick. “Big beats in inflation data like today’s will increase the pressure on Federal Reserve (Fed) Chair Jerome Powell’s characterization of inflation as ‘transitory’ and pull forward calls for tapering asset purchases.”

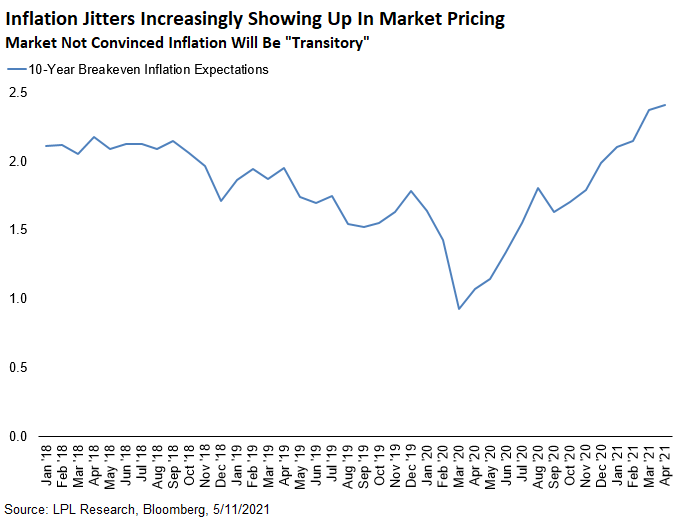

As seen in the LPL Chart of the Day, 10-year inflation breakeven rates, a measure of intermediate-term market price-based inflation expectations, have climbed steadily in the last few months. In fact, breakeven rates are now at their highest level since 2013. The market has digested this move higher in inflation expectations rather orderly so far without a major challenge to the latest monetary policy guidance. But, given inflation’s tendency to self-reinforce, markets could begin to grow bolder in their demands that the Federal Reserve change course and act sooner.

Much of the recent jump in inflation has to do with changes in the supply picture in our estimation, as the base effects and demand pickup were fairly well telegraphed. Surging input costs in supply chains are forcing companies to raise prices. Raw materials such as copper and lumber have been some of the most high profile culprits of late. Moreover, signs are pointing to the supply of labor becoming increasingly expensive and difficult to acquire. The most recent employment report showed that workers may require higher compensation to be enticed back into the workforce, especially while enhanced unemployment benefits continue. Finally, supply chain bottlenecks associated with quickly ramping up production are preventing companies from keeping up with surging demand in many cases, which places upward price pressures on existing supply.

While we forecast an inflation jump in the short-to-intermediate term, we do believe that longer term inflation will remain reasonably well contained. Market-based measures can tend to overshoot in both directions based on prevailing sentiment, and we think ultimately that Fed Chair Powell will be successful in preventing inflation from spiraling out of control. As mentioned, restarting the economy creates supply disruptions that feed into inflation, though in time these effects should self-correct. In fact, similar phenomena occurred exiting the 2008 recession, albeit on a more elongated timeline. Ultimately, though, inflation did not persist in earnest, as longer-term suppressors of inflation, such as globalization and technology, prevailed. We anticipate the story will end much the same this time around, but the ride may be bumpy in the meantime.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

If your representative is located at a bank or credit union, please note that the bank/credit union is not registered as a broker-dealer or investment advisor. Registered representatives of LPL may also be employees of the bank/credit union.

These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, the bank/credit union. Securities and insurance offered through LPL or its affiliates are:

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking # 1-05143632